Selecting a Winning Criminal Tax Lawyer is Crucial

The best criminal tax attorneys are often sought by taxpayers that believe “Winning is the Only Option.” Top criminal tax lawyers can make a real difference. Observe the results of the criminal tax trials of the best criminal tax attorneys. While most lawyers have never won a criminal tax trial while representing the Defendant, the top criminal tax lawyers often have a percentage of their criminal tax trials result in unanimous jury verdicts of NOT GUILTY on all counts for their clients. Listen to the unscripted testimonials of clients who have gone to trial, accused of tax fraud, describe in detail their experience. We welcome you to compare our trial results to any other lawyer’s or law firm’s.

Roanoke, Virginia United States v. Jeffrey Tharpe

Tax Evasion and Obstruction of IRS Verdict: NOT GUILTY

Each case is different with unique facts. Prospective clients may not obtain the same or similar results.

Numerous Not Guilty verdicts in federal criminal tax cases

Board Certified Expert in Taxation

LLM Master in Tax Law

Also a Certified Public Accountant (CPA)

Recognized by peers for tax knowledge and trial victories

Our firm has represented and successfully defended clients in federal criminal and tax matters throughout the United States for over 40 years. As tax lawyers in Miami, the successes are well known amongst practicing tax lawyers as well as Department of Justice, Tax Division attorneys. A sample of our firm's remarkable trial victories are listed below.

CRIMINAL JURY TRIAL

Each case is different with unique facts. Prospective clients may not obtain the same or similar results.

Trial Outcomes

Case Name Case Name

Case Number Case Number

Outcome Outcome

U.S. v. J.T.

20-CR-00020-Urbanski

Not Guilty on all Counts

U.S. v. S.G.

17-CR-00366-Adams

Not Guilty on all 30 Counts

U.S. v. N.M.

15-CR-20258-Lenard

Not Guilty on all 11 Counts

U.S. v. A.P.

15-CR-20096-Scola

Indictment Dismissed

U.S. v. R.R.

13-CR-20346-Ungaro

Not Guilty on all Counts

U.S. v. J.R.

13-CR-20346-Ungaro

Not Guilty on all Counts

U.S. v. J.M.

12-CR-60025-Williams

Not Guilty on all Counts

U.S. v. T.P.

09-CR-00038-Collier

Not Guilty on all Counts

U.S. v. H.C.

08-CR-20916-Graham

Not Guilty on all Counts

U.S. v. J.C.

08-CR-20044-Lenard

Hung Jury on all Counts

U.S. v. D.A.

04-CR-20190-Altonaga

Not Guilty on all Counts

State v. A.T.

F 04-CR-26073-Murphy

Not Guilty on all Counts

U.S. v. T.E.

98-CR-00511-Lenard

Not Guilty on all Counts

U.S. v. A.N.

18-CR-20280-Scola

Indictment Dismissed

U.S. v. C.U.

98-CR-00398-Seitz

Not Guilty on all Counts

For a detailed discussion of your specific case, please contact our office.

In addition to the cases referred to above, the law firm has successfully represented numerous persons under criminal investigation which our law firm successfully convinced the goverment not to file charges and to close the case.

RESPECTED REPUTATION

A reknown reputation as being one of the nation’s most successful and respected criminal tax attorneys

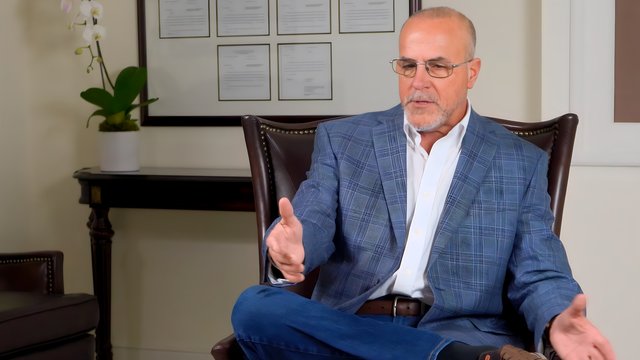

David M. Garvin is a Florida Bar board-certified tax specialist and concentrates his practice on white-collar crime and tax fraud defense, including tax evasion.

The results obtained for his clients speak for themselves, from grand jury investigations involving economic crimes to tax violations with full federal jury trials. The law firm's offices are located in Miami, Florida. However, we represent clients all over the United States.

Respected by His Peers

"I have done tax cases my entire career and I have co-defended dozens of them with everyone in town and I can tell you that David Garvin is THE man. There isn’t even a close second."

-- Alan S. Ross, partner Ross, Amsel, Raben, Nascimento, PLLC.

Google Reviews

When reliability and trustworthiness matter.

Alexandra Garvin and her legal team deliver an outstanding level of professionalism, precision, and strategic execution. From the very first interaction, it is evident that their firm operates with a deep understanding of both the legal framework and the business implications behind every case. Their attention to detail, responsiveness, and ability to navigate complex matters with clarity and confidence set them apart from typical legal services. Alexandra demonstrates not only strong legal expertise but also exceptional judgment, ensuring that every decision is aligned with the client’s best interest. What truly differentiates this firm is their commitment to results, transparency, and efficiency. They communicate clearly, execute decisively, and consistently exceed expectations. Without hesitation, I highly recommend Alexandra Garvin and her firm to anyone seeking top-tier legal representation backed by integrity, intelligence, and proven performance.

I’m very grateful to David M. Garvin and his team for the incredible support they gave my family. My father went through a very difficult IRS fraud case that lasted almost four years, and they stood by our side the entire time. Their professionalism, dedication, and constant guidance made a huge difference for us. We truly appreciate everything they did for our family and highly recommend David M. Garvin and his team.

I just want to write a thank you note to David Garvin and the job he did with my family’s business. We are extremely grateful for the outstanding legal support provided by David Garvin in resolving a complex federal matter involving the IRS after a former accountant created false W-2 forms connected to our business. What could have become a long and difficult court case was handled with exceptional professionalism, knowledge, and strategic care. Thanks to David Garvin’s expertise and dedication, the matter was successfully resolved in our favor without even having to go to court, which was truly remarkable and a tremendous relief for us. We would also like to sincerely thank Alexandra Garvin and Arlin Garvin, who work alongside him, for their guidance, professionalism, and support throughout the process. We are deeply thankful for their help and highly recommend David Garvin, Alexandra Garvin and his team to anyone in need of a trustworthy and highly capable federal legal representation.

My family and I are incredibly grateful to Attorney David M. Garvin and his amazing team for their dedication and support throughout one of the most difficult times we have faced. They helped us through a very complex IRS fraud case that lasted nearly four years, and during that entire time they stood by our side with professionalism, patience, and unwavering commitment. From the very beginning, Mr. Garvin and his team treated us with respect and truly cared about our situation. They worked tirelessly, guided us through every step of the process, and always made sure we understood what was happening. Thanks to their knowledge, integrity, and persistence, we were able to navigate this long and challenging process with confidence. We cannot thank them enough for everything they did for our family. If you are looking for an attorney who is honest, dedicated, and truly fights for his clients, I highly recommend David M. Garvin and his outstanding team.

I had the privilege of working with Attorney Alexandra Garvin on a very stressful IRS dispute, and I cannot recommend her highly enough. She was extremely professional, knowledgeable, transparent and trustworthy from day one. What stood out most was how personally invested she was in my case — she truly cared about achieving the best possible outcome. Thanks to her expertise, determination, and strategic approach she saved me hundreds of thousands of dollars. I am beyond grateful for her dedication and hard work. If you’re facing an IRS or any tax-related issue, you absolutely want Alexandra on your side.

LEGAL INSIGHTS & UPDATES

Latest Articles on Tax Law & Defense

May 9, 2023

Understanding AI-generated Tax Scams: A Letter to the IRS

Learn about the potential threat of AI-generated tax scams and the concerns raised in a letter to the Internal Revenue Service (IRS) from a group of concerned individuals. Discover what …

We use cookies and similar technologies for site analytics and advertising. See our Privacy Policy. Residents of certain U.S. states can opt out of the sale or sharing of personal information.

Privacy Choices

You can opt out of the sale or sharing of your personal information used for advertising. Learn more in our Privacy Policy.